Science is an uplift, performance marketing game

Most scientists are amateurs at selling entry level “masstige”

Brother Rumi writes …

A much older MIT professor and I like to compare notes on how to build winning organizations. We both validate each other’s financial thinking; I’m the younger industry upstart, and he’s the … well, you might know him.

Put the yadda yadda about the search for truth and teaching and all that aside. Scientists sell entry level luxury “masstige.” Know what a paper citation is worth to the author? $600 bucks on average. When you write a paper, you’re not Hermès, you’re Polène. [I’ll show you the math below.]

Real players – the time-and-time-again winners in science – run their organizations ruthlessly and have the business math of how to win at science down cold. And they never forget they are slinging purses that are just cerulean1 enough at this year’s Première Vision in Paris to be palatable for the industry to buy and match to consumer psychology of the moment.

Did you think science was intellectual? My friend, science is a fashion business in disguise.

Same deal with running a “creative” agency. Do you think Brian Collins doesn’t have his sector clocked? It’s not an accident that in an era of WPP Publicis etc. corporate peanut butter megamerger Brian’s tongue isn’t stuck to the roof of his mouth.

Only schmucks believe their field’s overt story because the revealed preferences speak the truth. You see the same phenomenon in weak companies and weak academic departments. Someone tells you they are driven purely by intellectual interest? You can be damn sure they are worried more about appearance than excellence.

If you want to be the very best you have to deeply understand the motivations of the humans around you, how their incentives reinforce their behaviors, and then turn those insights into a machine that routinizes greatness.

I’m sharing some of the things I’m teaching Sarah, my postdoc, and the early stage companies that I mentor because I’m in the business of building winners.

And I learned these lessons the very hard way. In order to play for Big Innovation you have to understand how to get “base hits” and just like in baseball, you should probably bunt a lot more than you’d think. I learned this stuff by staring into the suck, and God have I.

I figured there are very smart people in this world who are provably the best at what they do, and who am I to not imitate them and figure out how they do it?

Talent works harder than anyone else because they can. And when they do, it’s to a degree where it seems to rise to the level where they must.

Let’s unlock your talent and walk through the masstige calculation, as well as the ramifications of selling a kind of luxury good.

The grant renewal cycle creates a forward contract on research

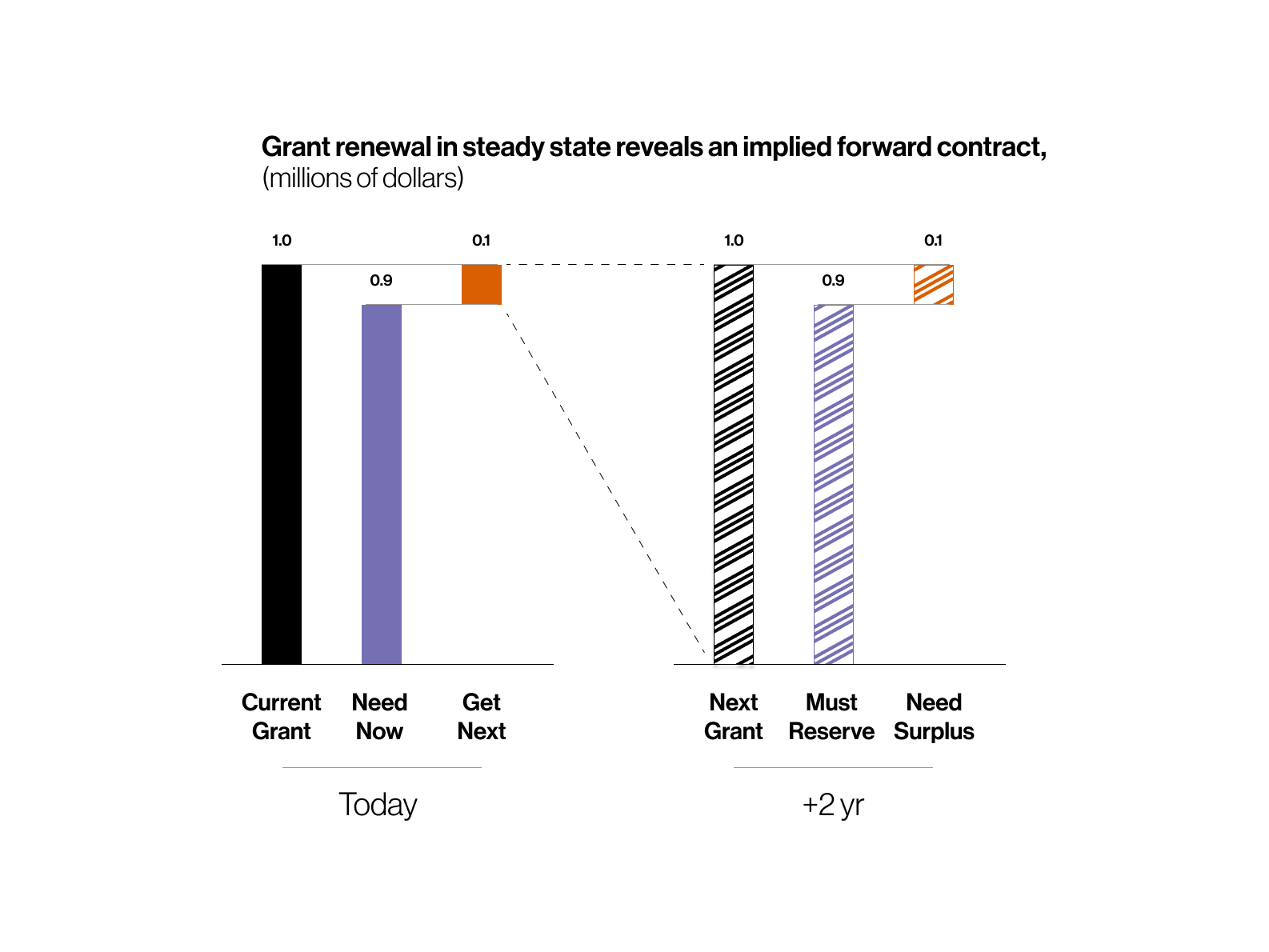

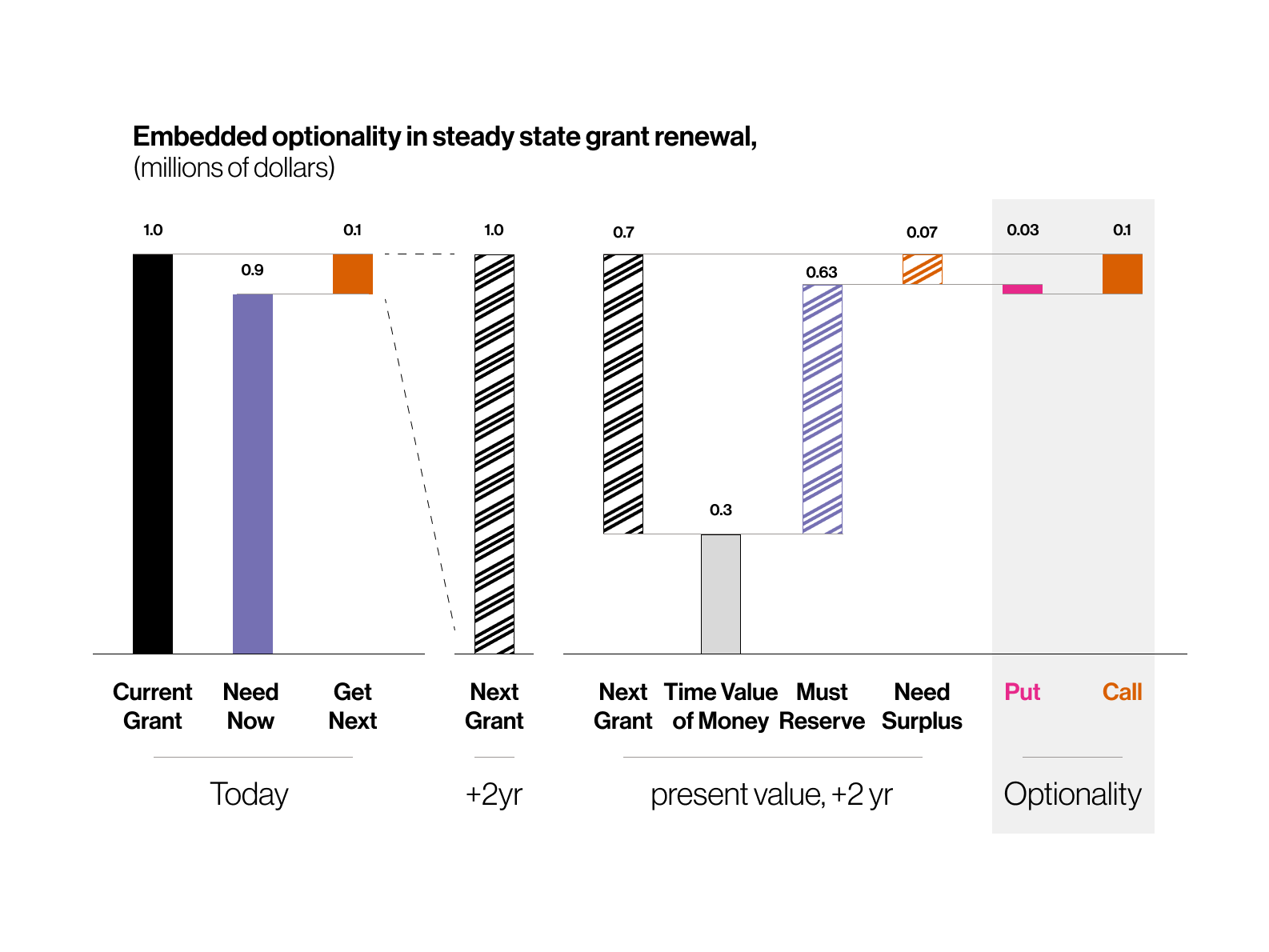

The trick is to use the last money to get the next money. The rule of thumb is that you use roughly 10% of the budget of the current grant to get the preliminary results you need to sell the next grant to funding agencies. [This is pretty much exactly the same math skilled senior managers use when they play the budget game.] This means that if you have a $1 million (written as $1mm) grant today, you have to achieve the aims of that grant with $0.9mm and use $0.1mm to collect the data you need for the next.

Now imagine your laboratory [/ a boutique firm] is in steady state, neither growing nor shrinking. That means the grant renewal cycle creates a forward on research where you break even2. If an R01 grant is $1 million ($1mm) let’s say you’ll get the money two years from now. We can split that again into two pieces, $0.9mm that is essentially an obligation and $0.1mm that’s the surplus.

Everything is relative to an opportunity cost. We could take that $100,000 and invest it in another worthwhile activity, like for example publishing. If we’re making good decisions then the value of the next grant in two years, which is not guaranteed for us to get, should be equal to the value we could otherwise create right now through publishing. Our goal is going to be to use this opportunity cost equivalence to figure out the value of publishing. So we need to find another way to estimate the opportunity cost.

What we know in general is that a forward for $1mm on delivery in two years is worth less than that now, and that’s determined by a discount rate:

Present Value of a $1mm forward in two years = $1 / (1 + rate)^(2 years).

If we know the right discount rate, we can price out the forward.

Up until 2024 our society acted like science has a roughly 20% return

You don’t capture all the value you create. A famous 1976 NASA study3 attempted to estimate the overall benefit that NASA investments had to the economy (and suggested a ridiculously high rate of return). [Economists call this “spillover” benefit.] Since then there have been many attempts to estimate the overall benefit; the most recent principled analysis I’ve found comes from the Dallas Fed4 where they argue that the benefit of $1 of nondefense R&D is essentially a $1.50 delayed perpetuity that matures in roughly 10 years. We can solve an equation to figure out what internal rate of return (IRR) this corresponds to:

Net Present Value = Payout / rate / (1 + rate)^(years - 1)

0 = 1.5 / r / (1 + r)^9 -1

Plugging those in, the rate r is approximately 20%. The government’s 10 year treasury bond (the “risk free rate”) is about 5% so we’re looking at a risk premium of about 15% – basically the same as venture capital. Let’s sanity check this against a big S&P500 company’s performance. Their typical risk premium is about 5% (for a total cost of equity of about 10%). In a recent NBER publication5 Peters et al. (2016) recently estimated a 6.6% multiple of a firm’s value through R&D. We can approximately convert this to an IRR:

IRR = weighted average cost of capital + depreciation rate x value gain / investment size

= 10% + 30% x 6.6% / 5% = 15% (approximately).

[The funny thing is that academics sneer at industrial scientists for being “commercial”, and in industry they love to sneer at academics for being “unapplied” but they have pretty much exactly the same performance on average. In my experience this is absolutely true. That’s why if you’re actually any good at your job, whatever your job is, you’re probably not an arrogant ass about it. In my experience kicking butt is kicking butt, it’s just a question of how you wish your total remuneration and impact to be configured. Personally, I want to build an enduringly mega impactful company, and that’s also aligned with my desire to build up the things and people around me.]

Now notice that the NIH portfolio was held flat in real terms until 2015 at ~$40bn / yr. The purpose of the NIH was to be able to tell a senator “we spent $X on your state” with a side effect of occasionally meriting some interesting research. [I’m saving what I really think of the NIH for a future article; let’s stick with a basic analysis here.]

These strongly suggest that R&D at the national level is explicitly managed for an average performance of about a 20% cost of equity (=15% risk premium) – exactly the same as a seed-stage VC investment.

The present value of the $1mm grant in two years is:

$1mm / 1.2^2 = $0.7mm

That means we’re investing $0.1mm now in the hope of getting $0.7mm two years later.

Most scientists do not do this calculation and suffer as a result. Top-tier scientists have an intuition for this analysis.

In fact we can even price out what a top-tier scientist’s performance is.

The existence of bridge funding implies a market price for how good a scientist is

Sometimes your grant ends before the next one is secured, and so departments can selectively offer bridge funding as a short term safety net. This is an investment, not a gift[, and it’s very hard to get money.]

Suppose the department head says,

“Listen, you’re doing awesome work, we’re going to offer you $50k as bridge funding because we believe in you.”

Bridge funding is a revealed preference on research quality.

Before we can get there we need to first make sure we price out whether we can get the money we need in the future to justify the investment of trying to get it.

There’s a built-in way to price out whether you’re going to be successful

We’ve previously discussed how forwards are linear instruments. It’s time for us to introduce nonlinearity and optionality.

Remember for a $1mm grant we’re going to spend ~10% of that (=$0.1mm) right now, and the remaining future $0.9mm is essentially an obligation / already spoken for. In reality we’re not confident about two things: whether we’ll get the grant, and what the dollar amount of the grant will be; in practice you negotiate with the funding agency. Let’s simplify and imagine that in two years we’ll find out how much the grant submission is worth above / below the $900k we’re going to need in case we get the grant.

Remember the $1mm grant in the future is only worth $0.7mm today to us; we have to pay an opportunity cost of $0.3mm. Because we’re in steady state we can simplify the math and see that 10% of the grant’s value in today’s terms is $0.07mm. This is smaller than the amount of money we’re putting in today.

This means we’ve split a linear instrument – the forward – into two nonlinear instruments, a call option (which is the payoff we get above $0.9mm; in present terms that’s $0.63mm) and a put option (the payoff less than $0.9mm); we usually just say “call” and “put” without the option part. This means we’re pricing the possibility of not having enough money as

Call - Put = Present Value of Forward - “Obligation” (which is called the strike)

The call is $0.1mm (that’s our hope for the good outcome), and so that means the put is $0.03mm; these options have two-year maturities.

Bridge funding is an insurance policy

Now I can tell you that every single department head who knows what they are doing has a mental model something like this.

“I’m going to give Professor Tryhard between $30k to $50k if they aren’t leaning over their skis, and maybe consider funding a moonshot proposal with $50k - $75k. If they need less than $30k then this had better be a slam dunk.”

In fact if they can’t bridge you $30k for a semester then either they are broke or they don’t believe in your work.

Notice that this $30k is exactly the same price as the put we just estimated by assuming a general spillover return that you can capture on the value of your research “to society” at about a 20% cost of equity.

I don’t want to wave my hands and say something “woo” like, “oh the invisible hand of the market!” but this really is yet another example of how the most serious players are much more rational about pricing things than the average joes realize. At MIT and other top universities they do not fuck this calculation up, and the best department heads know this math inside out.

All the best scientists I know have at least an intuition for the numbers, if not the math, behind this because how the hell else do you reliably excel at your job?

I can also say the converse. Weak departments fuck these calculations up all the time, and that’s why they stay weak.

Let me go further.

The fastest way to know that your brand sucks is if the stewards of the brand don’t get that the market is always pricing your performance, especially for the “soft” stuff, because the soft stuff matters more than what you think is the “hard” stuff.

By the way, you might have noticed that if we think of the $0.07mm as an expected value on getting the next $0.1mm (heads you get enough / tails you don’t) then it looks like a 70% probability of success. This is called a risk neutral probability and you must NOT fall into the trap of taking it seriously; we talked about this previously as well. Why? Well among other considerations we estimated the 20% discount rate by a general argument. If a more careful analysis for the particular subfield of science etc. plus adjusting for the seniority and “credit worthiness” of a particular scientist gave us a let’s say 10% discount rate then the risk-neutral probability would be 83%, and a 30% discount rate would give us a 60% probability. We really do expect this kind of spread to exist. Plus, as we alluded to last time, risk neutral probabilities imply a lot of assumptions that do not hold true in the real world marketplace. We can’t allow ourselves to fall into the trap of “woo, invisible hand” thinking. The markets are not perfect.

Publications are priced by opportunity costs

The forward on a $1mm grant is worth $700k today. That means the time value of money is $300k. If we are exactly as productive in the meantime in terms of brand value that we capture from the positive value to society we create through publications, then the publications from the state of our knowledge today have to be worth $300k, too.

The estimates range widely but there’s roughly 500 citations that arise per R01 grant6. That means we can calculate the value of an average citation to be:

$300k / 500 = $600 per citation.

Put your marketing hat on. If you’re selling a $600 purse by converting on 500, you needed at least 5,000 touches (/ readers), and that probably required about 50,000 as reach – we’re using the usual 1 : 10 : 100 multipliers.

Guess what Nature’s individual paid subscriber base is? Roughly 50,000. Coincidence? I think not.

Now let’s borrow some numbers from other places. Nature charges roughly $15k to publish a paper. Let’s suppose you get two Nature papers out in the two years you’ve got to cover as an opportunity cost, one per year. That $30k looks suspiciously like a 10% value capture on the $300k value of publications to you.

Coincidence? Surely not.

If we estimate the adstock decay rate / retention rate of our marketing through publications:

$300k = $30k / (1 - λ)

=> λ = 90%

Which implies the marketing decay rate is 10%. We’re estimating the half-life of a Nature paper for people to “buy” the ideas in it is about 6.5 weeks.

The rule of thumb in marketing mix modeling is that masstige luxury has a retention rate of about 80%.

I don’t think these are coincidences.

It doesn’t have to be a calculation to be calculated bets.

Nature / Science / Cell are selling masstige as entry level luxury goods.

Look, whenever people tell you that you can’t measure uplift, you can tell them that even in science – which is an area of human endeavor that proclaims itself to be free of market forces – is dead on the money all about uplift.

If you aren’t measuring uplift you aren’t trying hard enough to think very simply and clearly.

You must start with the heart – people reveal their true selves and buy things emotionally – and over time the prices can work out to be logical. The marketers who understand the math of yearning excel regardless of whether they think of themselves as marketers. And so will scientists who understand the art of selling.

Why not be great on purpose?

=Brother Rumi

Yes, I’m making a Devil Wears Prada reference; give me love.

It’s economically equivalent to a forward contract, but we don’t literally write forwards. Maybe we should ;)

“The Economic Impact of NASA R&D Spending” https://ntrs.nasa.gov/api/citations/19760017002/downloads/19760017002.pdf

“The Returns to Government R&D: Evidence from U.S. Appropriations Shocks” https://www.dallasfed.org/research/papers/2023/wp2305

“Dynamic R&D Choice and the Impact of the Firm’s Financial Strength” https://www.nber.org/papers/w2203

Agrawal & Tu (2022) doi:10.1007/s11606-021-06659-y

| A guest post by

|

I truly enjoyed this piece.

I'm going to ponder this for a while. As I did after receiving the draft from @Rumi yesterday.

I like the way of reasoning, the topic however is too alien for me to wrap my head around easily.

And includes several sub-topics.

As I mentioned to someone else:

Fortunately I learned that there is a huge difference between not knowing and ignorance, and can always move my mind from “I know” to “there is more to uncover”.